/

•

•

Detailed stories on technology startups, business and economic current affairs.

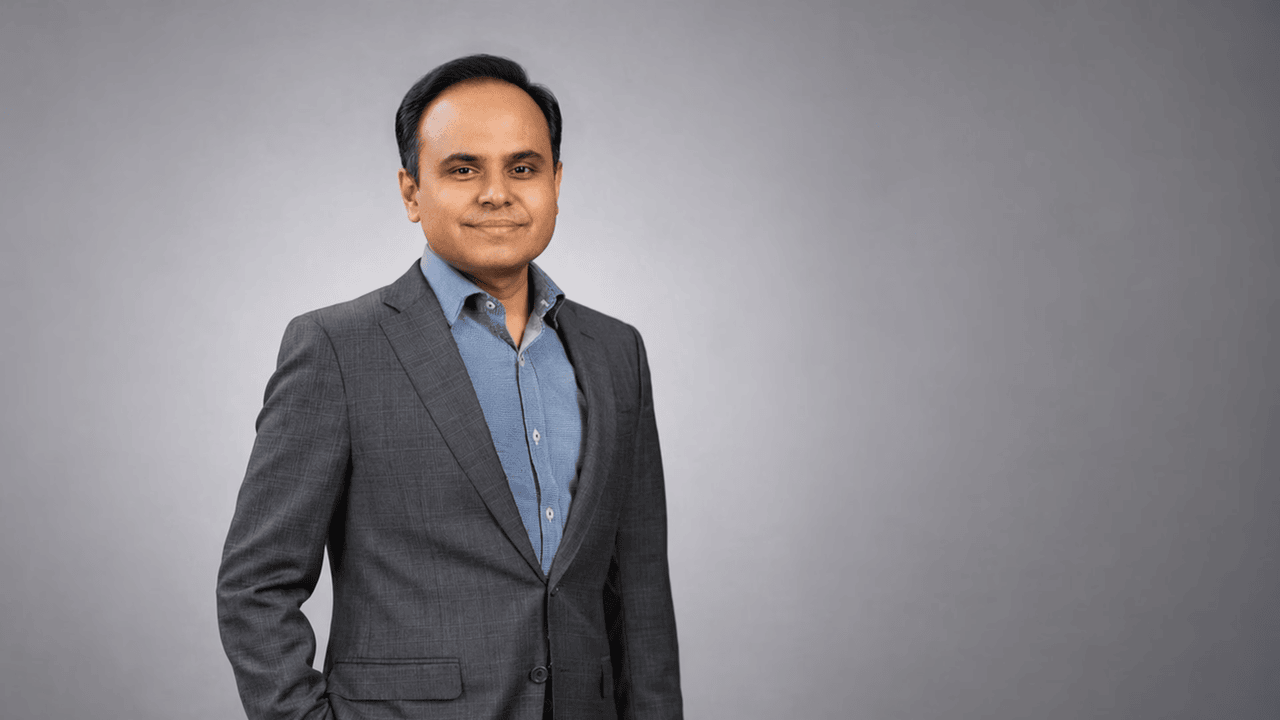

Under its current CEO, the lender has witnessed a turnaround in the last four years. Yet, its rising exposure to corporate loans and high levels of stressed assets remain concerns.

Editor's note: April 2017. Bank of Maharashtra had just declared its fourth quarter results for the 2016-17 fiscal year and they were not a pretty sight. Its gross bad loan ratio was at 16.93%, and had risen by 65% over a year. The bank’s capital was eroding fast and its capital adequacy ratio had plummeted to 11.18%—well below the Reserve Bank of India’s 12% minimum. The net loss for the year was over Rs 1,300 crore; every quarter in the fiscal had thrown up a loss. A concerned RBI had no option but to intervene. With depleting capital, rising bad loans and mounting losses, the bank was fast sliding to a point of no return. So, in June 2017, it placed it under the prompt corrective action, or PCA, framework—a structured early-intervention mechanism for banks that become undercapitalized due to poor asset quality, or vulnerable due to loss of profitability. As a consequence, strictures were placed on the bank’s lending activities. A year and a half later, in December 2018, when the current managing director and CEO of the bank—A.S. Rajeev—took charge, …

Under its current CEO, the lender has witnessed a turnaround in the last four years. Yet, its rising exposure to corporate loans and high levels of stressed assets remain concerns.

Editor's note: April 2017. Bank of Maharashtra had just declared its fourth quarter results for the 2016-17 fiscal year and they were not a pretty sight. Its gross bad loan ratio was at 16.93%, and had risen by 65% over a year. The bank’s capital was eroding fast and its capital adequacy ratio had plummeted to 11.18%—well below the Reserve Bank of India’s 12% minimum. The net loss for the year was over Rs 1,300 crore; every quarter in the fiscal had thrown up a loss. A concerned RBI had no option but to intervene. With depleting capital, rising bad loans and mounting losses, the bank was fast sliding to a point of no return. So, in June 2017, it placed it under the prompt corrective action, or PCA, framework—a structured early-intervention mechanism for banks that become undercapitalized due to poor asset quality, or vulnerable due to loss of profitability. As a consequence, strictures were placed on the bank’s lending activities. A year and a half later, in December 2018, when the current managing director and CEO of the bank—A.S. Rajeev—took charge, …

The central bank’s shift to a 100% collateral requirement threatens to erode leverage, reduce volumes and force a consolidation across prop desks.

High returns, RBI-regulated comfort, and easy withdrawals drew investors in. Now, with repayments drying up, the fintech platform, its NBFC partner, and the regulator are pointing fingers—leaving customers to chase their own money.

The RBI’s unusually harsh order raises deeper questions about management credibility—and whether investors should take assurances at face value.

The central bank’s shift to a 100% collateral requirement threatens to erode leverage, reduce volumes and force a consolidation across prop desks.

High returns, RBI-regulated comfort, and easy withdrawals drew investors in. Now, with repayments drying up, the fintech platform, its NBFC partner, and the regulator are pointing fingers—leaving customers to chase their own money.

The RBI’s unusually harsh order raises deeper questions about management credibility—and whether investors should take assurances at face value.