/

•

•

Detailed stories on technology startups, business and economic current affairs.

The watch retailer, with a focus on quality and customer experience, now has a near 20% share of the luxury market. It remains to be seen if it can retain investors’ interest.

The watch retailer, with a focus on quality and customer experience, now has a near 20% share of the luxury market. It remains to be seen if it can retain investors’ interest.

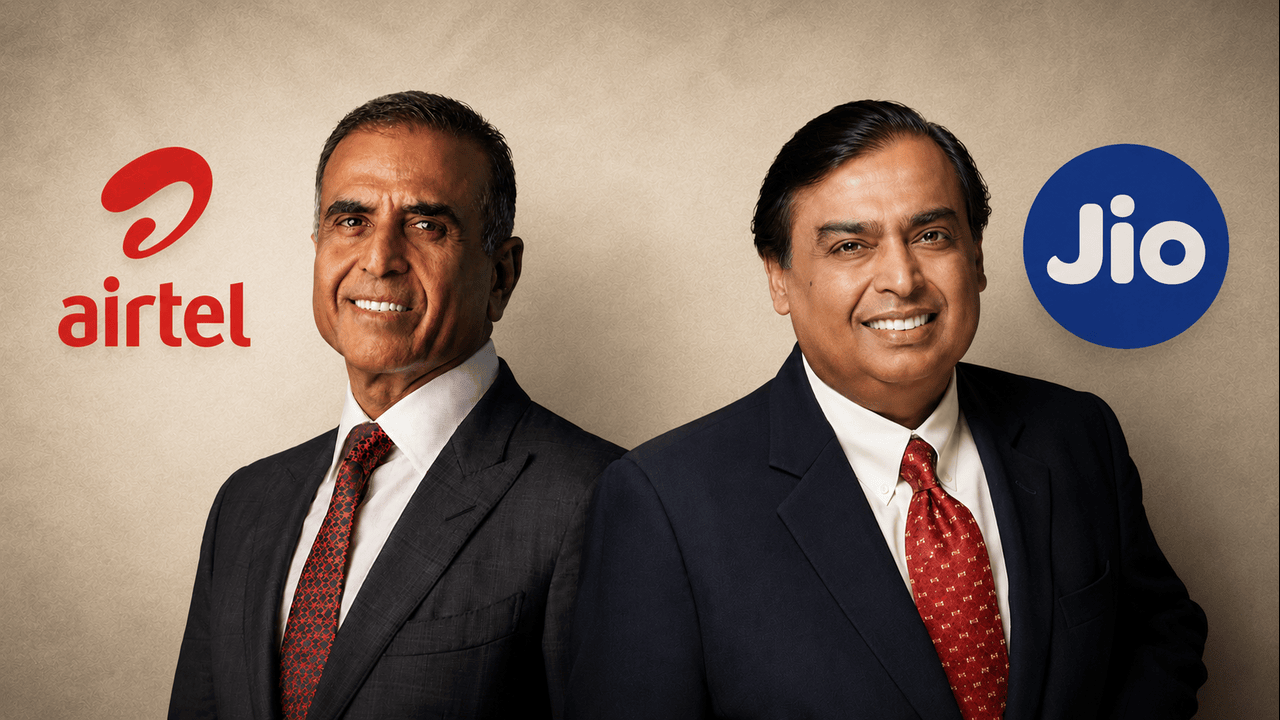

FY26 numbers show that Airtel is stealing a march on its larger rival on most counts and is unrelenting in its ambition, casting a cloud on Jio’s valuation.

Surprisingly strong metrics alongside aggressive expansion mask a lurking balance-sheet risk. Moreover, competition is not going to be kind to the retail giant any time soon.

Telecom and retail both continue with their ‘hit and miss’, while O2C delivers an unsurprisingly poor performance in Q4. This is a year RIL will be glad to see the back of.

FY26 numbers show that Airtel is stealing a march on its larger rival on most counts and is unrelenting in its ambition, casting a cloud on Jio’s valuation.

Surprisingly strong metrics alongside aggressive expansion mask a lurking balance-sheet risk. Moreover, competition is not going to be kind to the retail giant any time soon.

Telecom and retail both continue with their ‘hit and miss’, while O2C delivers an unsurprisingly poor performance in Q4. This is a year RIL will be glad to see the back of.