/

•

•

Detailed stories on technology startups, business and economic current affairs.

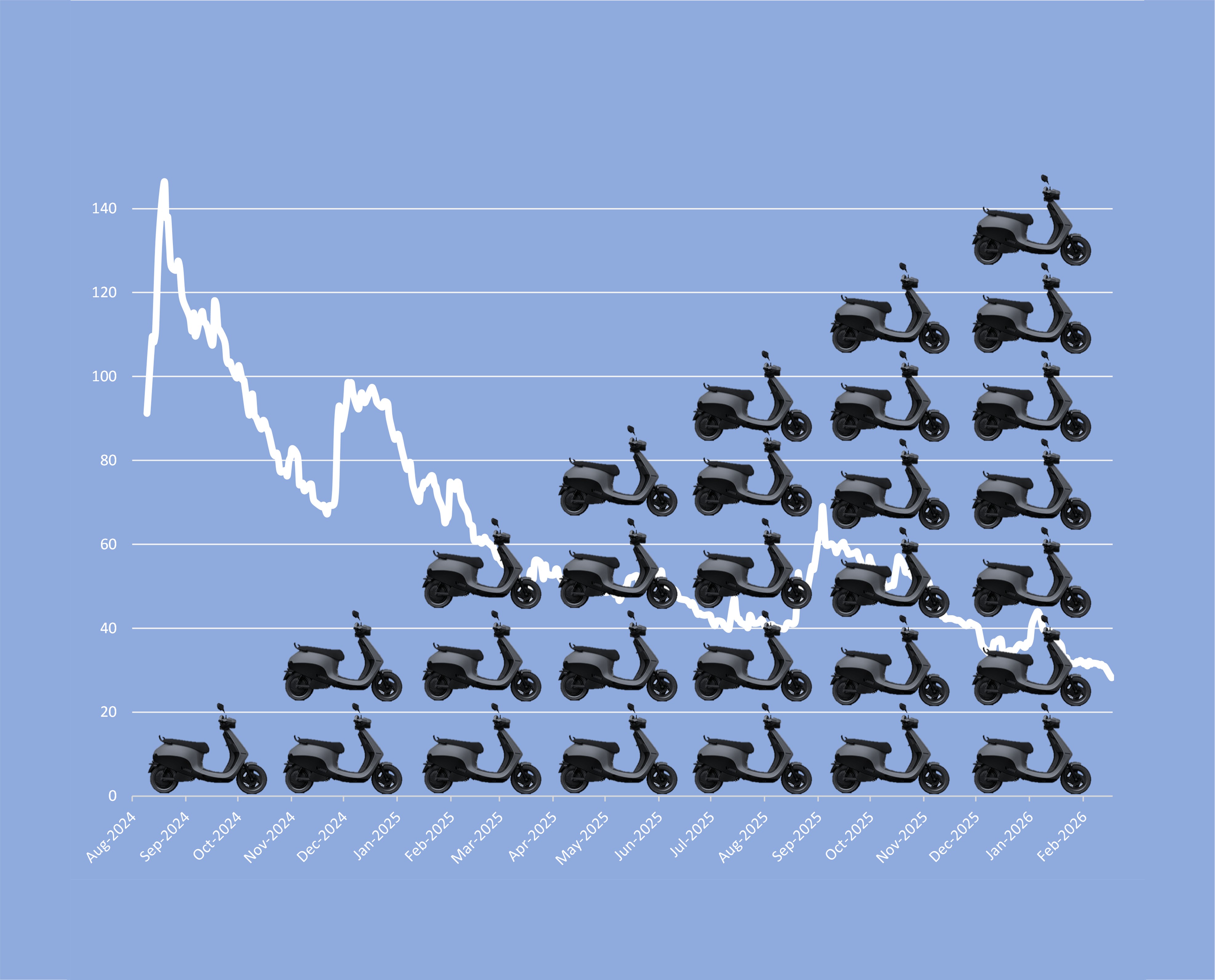

While its peers headed for the exit, the fund house doubled down on the falling stock. The contrarian call now looks expensive—and risky.

While its peers headed for the exit, the fund house doubled down on the falling stock. The contrarian call now looks expensive—and risky.

The regulator’s shift to an auction-based close was meant to curb manipulation and mirror global markets. Instead, it has run into thin participation that is only amplifying distortions and volatility.

FY26 numbers show that Airtel is stealing a march on its larger rival on most counts and is unrelenting in its ambition, casting a cloud on Jio’s valuation.

Surprisingly strong metrics alongside aggressive expansion mask a lurking balance-sheet risk. Moreover, competition is not going to be kind to the retail giant any time soon.

The regulator’s shift to an auction-based close was meant to curb manipulation and mirror global markets. Instead, it has run into thin participation that is only amplifying distortions and volatility.

FY26 numbers show that Airtel is stealing a march on its larger rival on most counts and is unrelenting in its ambition, casting a cloud on Jio’s valuation.

Surprisingly strong metrics alongside aggressive expansion mask a lurking balance-sheet risk. Moreover, competition is not going to be kind to the retail giant any time soon.