/

•

•

Detailed stories on technology startups, business and economic current affairs.

One of India’s largest banks has gone all in on a technology-first revamp of everything from internet banking to trade finance.

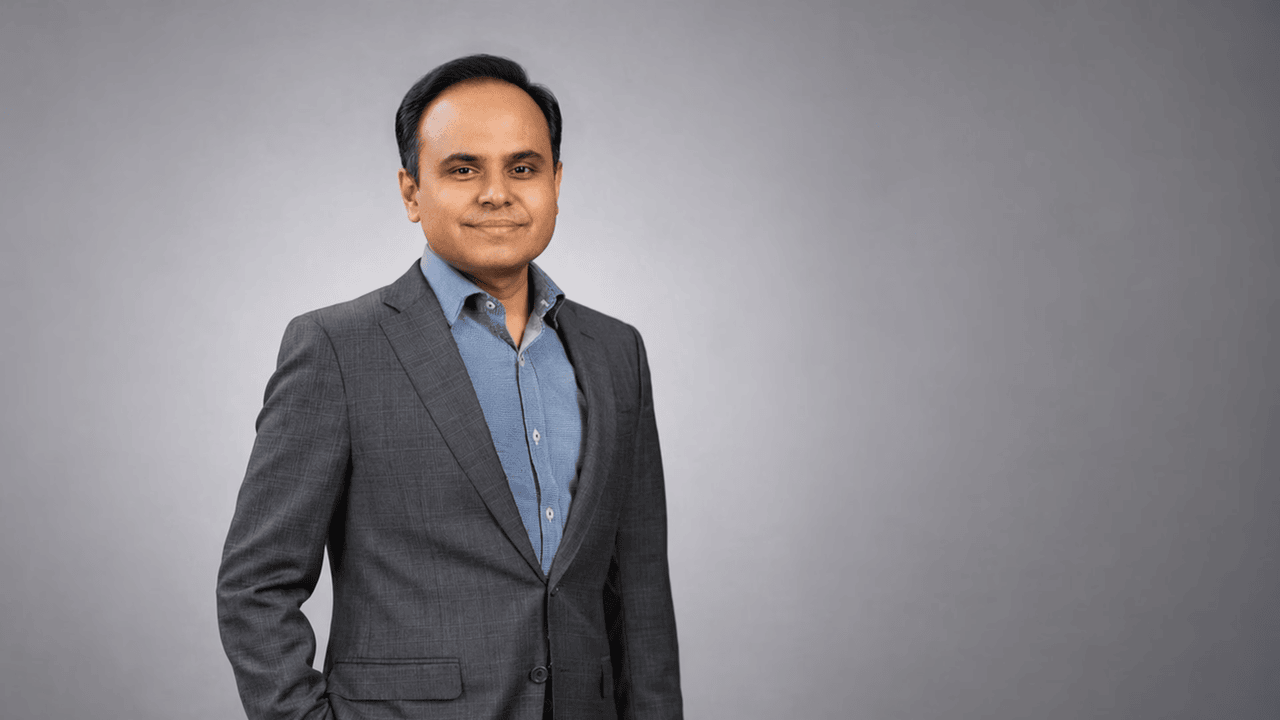

Editor's note: Early on in his stint as chief executive officer of ICICI Bank, Sandeep Bakhshi decided that he would use technology to transform—and clean up—one of India’s largest lenders. And he had no time to waste; the change had to start taking effect immediately. The Chanda Kochhar episode, which saw Bakhshi’s predecessor step down over allegations of fraud and undisclosed conflict of interest, had revealed serious corporate governance shortcomings at the bank. Many wondered if it could ever get over what was one of the most high-profile scams in Indian banking history. If customer and investor confidence were low, industry circumstances weren’t helpful either. The Indian banking system was in dire straits. Even before the demonetization shock waned, banks had to deal with piles of bad loans. Months before Bakhshi took over in October 2018, ICICI Bank had reported its highest non-performing asset numbers ever. Then infrastructure financing giant IL&FS collapsed, triggering a debt market crisis with several non-bank lenders and real estate developers defaulting on their bank loans. Three years on, much has changed. Under Bakhshi, who had led the …

One of India’s largest banks has gone all in on a technology-first revamp of everything from internet banking to trade finance.

Editor's note: Early on in his stint as chief executive officer of ICICI Bank, Sandeep Bakhshi decided that he would use technology to transform—and clean up—one of India’s largest lenders. And he had no time to waste; the change had to start taking effect immediately. The Chanda Kochhar episode, which saw Bakhshi’s predecessor step down over allegations of fraud and undisclosed conflict of interest, had revealed serious corporate governance shortcomings at the bank. Many wondered if it could ever get over what was one of the most high-profile scams in Indian banking history. If customer and investor confidence were low, industry circumstances weren’t helpful either. The Indian banking system was in dire straits. Even before the demonetization shock waned, banks had to deal with piles of bad loans. Months before Bakhshi took over in October 2018, ICICI Bank had reported its highest non-performing asset numbers ever. Then infrastructure financing giant IL&FS collapsed, triggering a debt market crisis with several non-bank lenders and real estate developers defaulting on their bank loans. Three years on, much has changed. Under Bakhshi, who had led the …

The Rs 250 SIP was launched last year by the former SEBI chairperson with one clear goal: financial inclusion. More than a year later, the much-hyped scheme doesn’t seem to have caught on with MF investors.

Europe’s largest fintech firm has its sights set on the Emirates. What can we expect?

The Mideast tech giant is scaling back verticals in Saudi Arabia and possibly rethinking global operations.

The Rs 250 SIP was launched last year by the former SEBI chairperson with one clear goal: financial inclusion. More than a year later, the much-hyped scheme doesn’t seem to have caught on with MF investors.

Europe’s largest fintech firm has its sights set on the Emirates. What can we expect?

The Mideast tech giant is scaling back verticals in Saudi Arabia and possibly rethinking global operations.